PARAMOUNT INSURANCE BROKERS

Medicare Advantage

Medicare Advantage, also known as Medicare Part C, is a health insurance plan provided by private companies approved by Medicare. It offers at least the same coverage as Original Medicare – Part A and Part B. But also, Medicare Advantage gives some additional benefits that Original Medicare does not provide. The most often added benefit is prescription drug coverage (Part D), which is included in almost every Part C plan.

These additional benefits can sometimes be provided at no additional cost to you. This is possible because Medicare actually pays the insurance company a set amount for providing your healthcare coverage.

So, let’s take a look at the eligibility, enrollment, and benefits of an Advantage plan.

MEDICARE ADVANTAGE ENROLLMENT

If you are eligible for Medicare, then you will want to know when is the time for enrollment. There are specific enrollment times during which you can enroll in a Medicare Advantage plan:

Initial enrollment period — Your initial enrollment period is a seven-month period that starts three months before the month you turn 65 and ends three months after the month you turn 65. If you are under 65 and receive Social Security disability, you qualify for Medicare in the 25th month after you begin receiving your Social Security benefits. If that is how you are becoming eligible for Medicare, you can enroll in an Advantage plan three months before your month of eligibility until three months after you became eligible.

Open enrollment period — Also known as annual enrollment or AEP, the open enrollment period for Medicare Advantage is from October 15 through December 7 every year. Coverage for the Part C plan you choose during this time will start on January 1 next year. During this time, you can also add, change, or drop current coverage.

Medicare Advantage Open Enrollment Period — During this MA Open enrollment period, you are able to change from one Advantage plan to another or drop it to return to Original Medicare.

Special Election Period — There are several things that can trigger a special election period and they are unique to an individual. It is best to speak to a licensed Medicare insurance agent to find out if you qualify for a special election period. However, there are a few common instances we can talk about. Such as, if you move outside your Medicare Advantage plan’s service area, qualify for extra help (such as a program that helps pay for your prescription drugs), or move into a nursing home you might qualify for a special election period. During this time you can make changes to your Advantage plan or return back to Original Medicare.

MEDICARE ADVANTAGE COVERAGE

Medicare Advantage coverage for inpatient care, in general, is covered by Medicare Part A. Regarding Part C, it covers the same services as Medicare Part A, including inpatient hospital care and inpatient care in the skilled nursing facility. Part C also covers Home health care, but hospice care benefits remain under Original Medicare (Part A and B).

As for coverage for outpatient care, which is covered by Part B in general, Medicare Advantage covers the same benefits as Part B, including visits to primary care doctors or specialists, tests and x-rays, emergency ambulance services, mental health services (both inpatient and outpatient), durable medical equipment, vaccines, physical or occupational therapies, and speech and language pathology.

There are a few extra benefits that Medicare Part C can cover, but Original Medicare does not. Some of these services that Medicare Advantage may include as extra benefits are: Routine dental, vision, and hearing care, fitness benefits such as exercise class (SilverSneakers membership), emergency medical assistance while traveling outside the U.S., and allowance to buy health care products. But not all Medicare Part C plans cover these mentioned extra benefits, as well as they are not limited to them.

MEDICARE ADVANTAGE COSTS

There is a wide range of plan costs. Many people choose low-cost or free plans, and $0 Medicare Part C plans are available in 49 states. On the other side, some plans can cost several hundred dollars per month. Expensive plans usually provide better benefits such as a broader network of medical providers, more coverage for specialized care, or better cost-sharing benefits.

Medicare Part C costs are determined by several factors, such as premiums, deductibles, copayments, and coinsurance. These amounts can range from $0 to hundreds of dollars for monthly premiums and yearly deductibles. But most of your Part C costs will be determined by your chosen plan. Here below are some of the most common factors affecting Part C plan cost:

- Premiums: Some Medicare Part C plans are free, meaning they don’t have a monthly premium. But even if it is a $0 premium, you may still owe the Part B premium.

- Deductibles: Most Medicare Part C plans have both a plan deductible and a drug deductible. Some of the free Medicare Advantage plans offer a $0 plan deductible.

- Copayments and coinsurance: Copayments are amounts you will owe for every doctor’s visit or prescription drug refill. Coinsurance amounts are any percentage of services you must pay out of pocket after your deductible has been met.

- Plan type: The type of plan you choose can also have an impact on how much your Part C plan may cost.

- Out-of-pocket maximum: One advantage of Medicare Part C is that all plans have an out-of-pocket maximum.

- Lifestyle: Most Medicare Advantage plans are location-based because they depend on the provider`s network. This means that if you travel often, you may find yourself stuck with out-of-town medical bills.

- Income: Your yearly gross income can also factor into how much you will pay for your Medicare Part C costs. Individuals with higher incomes will have higher Medicare costs.

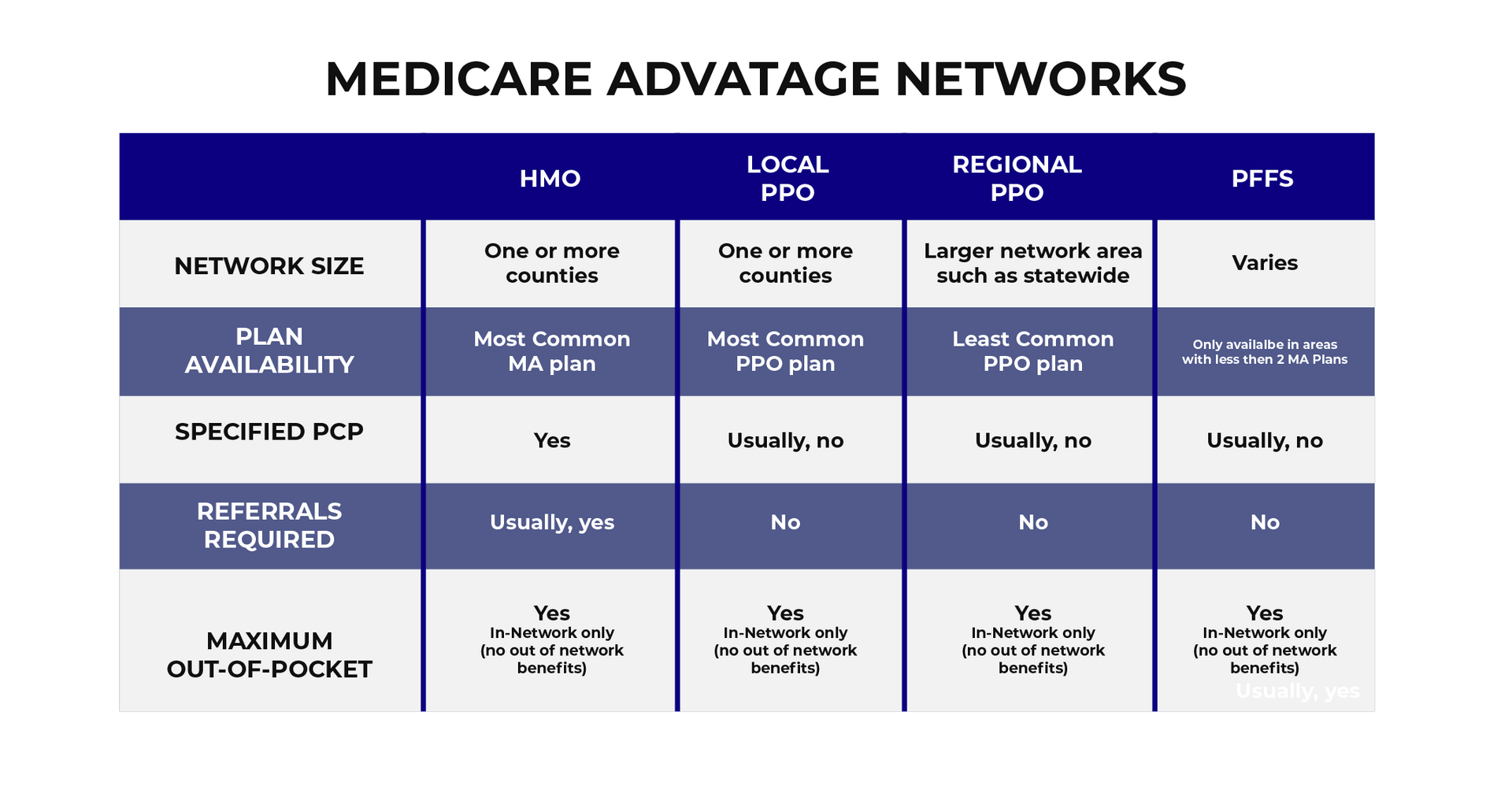

TYPES OF MEDICARE ADVANTAGE PLANS

There are four main types of Medicare Advantage plans offered: Health Maintenance Organization (HMO) plans, Preferred Provider Organization (PPO) plans, Private Fee-for-Service Plans (PFFS), and Special Needs Plans (SNP).

There is also a Medicare Advantage Medical Savings Account Plan (MSA), which covers benefits from Original Medicare and gives additional benefits. But MSA is specific that they come as a high deductible health plan with a bank account to help you pay for your medical costs. For a detailed breakdown read out a blog about Medical Savings Account plans.